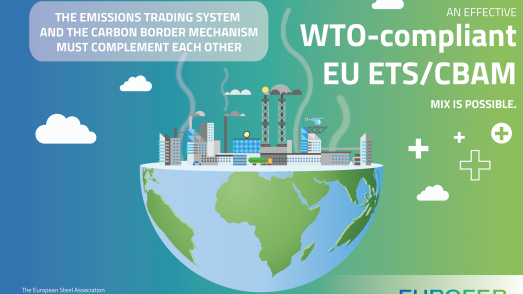

A Carbon Border Adjustment (CBA) mechanism is a tool to support the EU's climate leadership by reflecting the carbon intensity of products imported into the EU, such as steel. This mechanism is important because EU producers have the highest environmental and climate protection goals in the world - and higher production costs that accompany this effort.

The European steel industry is therefore at very high risk of carbon leakage - the loss of sales to cheaply-priced, carbon-intense imports. Avoiding the risk of carbon leakage is a pre-condition for preserving both the environmental integrity of EU climate policy and industrial competitiveness since it contributes to reducing emissions at a global level while maintaining jobs and investments in Europe. This will also be instrumental in facilitating the social acceptance of EU leadership in climate ambition.

The European Green Deal underlines that the risk of carbon leakage can materialise in different forms, 'either because production is transferred from the EU to other countries with lower ambition for emission reduction, or because EU products are replaced by more carbon-intensive imports'. As long as there is no international binding agreement with a global carbon price and equivalent efforts, it is essential that the EU legislation adopts effective measures that avoid all forms of leakage in the short and medium terms.

The carbon border adjustment measure should be applied for a transition period until breakthrough technologies reach sufficient market penetration and CO2-lean products represent a critical mass in the market. It represents a broader contribution to a clean planet, as it is also an effective tool of political diplomacy to foster climate ambition in third countries so that deeper emission reductions are delivered globally.

Brussels, 12 June 2026 - Europe's steel industry has noted improvements made by EU ministers to the proposed reform of the Carbon Border Adjustment Mechanism (CBAM), but warns loopholes remain that could weaken both Europe's climate ambitions and industrial competitiveness.

The signatories call on the European Parliament and Council to ensure an effective and broad extension of the CBAM to relevant steel and aluminium intensive downstream industries.

Brussels, 3 April 2026 – The European Steel Association (EUROFER) has set out proposals to improve the EU’s Carbon Border Adjustment Mechanism (CBAM), just as the system enters a decisive new phase with the publication of the first carbon certificate prices expected on 7 April 2026.

The European Steel Association (EUROFER)

172 Avenue de Cortenbergh

1000 Brussels

Belgium

Email: mail@eurofer.eu

Phone: +32 (0) 2 738 79 20